The Largest “Junk Fee” in Housing That No One Is Talking About

February 20, 2026

The regulatory spotlight on the rental industry has never been brighter. From the FTC’s crackdown on hidden costs to state-level mandates for total transparency, the message to property managers is clear: if a fee doesn’t provide clear value to the resident, it’s a liability.

We’re seeing a wave of scrutiny targeting valet trash, mandatory technology bundles, and administrative "convenience" fees. These are being framed—rightly or wrongly—as hidden rent hikes.

But while the industry scrambles to audit its fee folders, the largest "junk fee" in residential real estate is hiding in plain sight. It’s not an added charge on a ledger; it’s a massive transfer of value away from the renter.

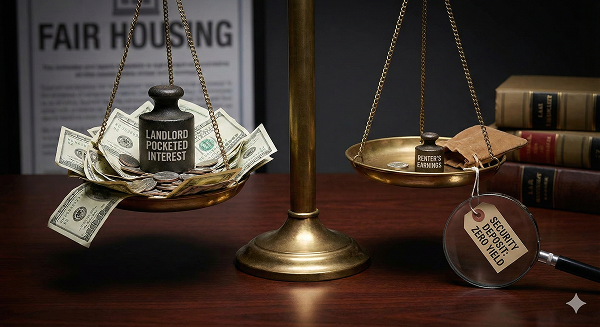

It’s the lost interest on security deposits.

The Billions Sitting Idle

Security deposits are, by legal definition, the resident’s funds. They are a good-faith asset held for the duration of a lease. Yet, across millions of units, that capital sits in non-interest-bearing escrow accounts or generates interest that rarely makes its way into the renter’s pockets.

Think about the scale: billions of dollars in resident capital are generating value for everyone except the people who actually own the money.

In an era where "fairness" is the new regulatory benchmark, holding $2,000 of a resident's money for three years without returning the yield on that capital is increasingly difficult to justify.

Why the Status Quo is Failing

For decades, property managers avoided paying interest because the administrative cost of doing so was higher than the interest itself. Calculating pro-rated interest, filing 1099-INTs, and cutting separate checks for $12.41 was a manual nightmare that no accounting team wanted to touch.

To solve this, many turned to deposit alternatives—surety bonds or deposit insurance—but these products replace a refundable deposit with a non-refundable fee. From a regulator's perspective, replacing a resident's asset with a non-refundable "junk fee" that offers the renter zero coverage is moving in the wrong direction.

The "Fair Housing" Evolution

Modernizing the security deposit isn't just about avoiding a fine; it’s about brand alignment. Today’s renter is more financially literate than ever. They see high-yield savings rates in their banking apps and then look at their security deposit sitting in a "black box" for 12 months.

The expectation is shifting from: "Will I get my money back?" to "Why isn't my money working for me while you hold it?"

Property management leaders are realizing that providing transparency and yield isn't just a "perk"—it’s a competitive advantage that builds trust at the most sensitive points of the resident lifecycle: move-in and move-out.

Transparency as a Strategy

At Whale, we believe the solution to the "junk fee" era isn't more fees—it’s more transparency. The future of the industry depends on returning the economics of the deposit to the rightful owner.

- No Resident Charges: Residents shouldn't pay a fee to "not pay" a deposit. They should simply keep their money in a way that works for them.

- Native Yield: By moving deposits into renter-owned accounts, the resident earns market yield on their own capital automatically.

- Zero Admin: Because the account stays in the resident's name, the landlord is removed from the tax reporting and interest calculation loop entirely.

The industry is moving toward a "what you see is what you get" model. Operators who continue to treat security deposits as a source of friction or hidden float will find themselves on the wrong side of both the law and resident sentiment.

The future of deposits is simple—clean, compliant, and transparent. And that’s exactly how it should be.